.svg)

.svg)

.jpeg)

.png)

Digital payments in the UAE are expected to reach $70 billion in 2024. The UAE specifically is a global retail hub where people from all over the world come to shop and have vacations, which is why it is important for a small business operating in the region to offer a variety of payment options to your customers including cards, e-wallets or payment links. If you are a small business owner looking to digitize your payment options, then you should start with getting an understanding of payment processors.

So, what is a payment processor, and why does it matter to your business? For your convenience, we have put together a guide on what a payment processor is and how to pick the best one for your small business in the UAE. Whether you have an an offline or online business, this article will provide you with all the tips and concepts to digitize your payment process.

What Is a Payment Processor?

A payment processor is a type of service or technology provider that transfers money from your customer's bank account to your business bank account. In basic terms, it is the intermediary between your business bank account and the buyer payment method (which can be a credit card or digital wallet).

When a customer makes a payment—whether online or in person through a POS—a payment processor ensures the transaction is secure, authenticated, and completed seamlessly. Without it, you wouldn’t be able to accept modern payment methods like cards, mobile payments, or online transfers.

For businesses in the UAE, using a reliable payment processor is essential to cater to a digitally savvy consumer base accustomed to fast and secure transactions.

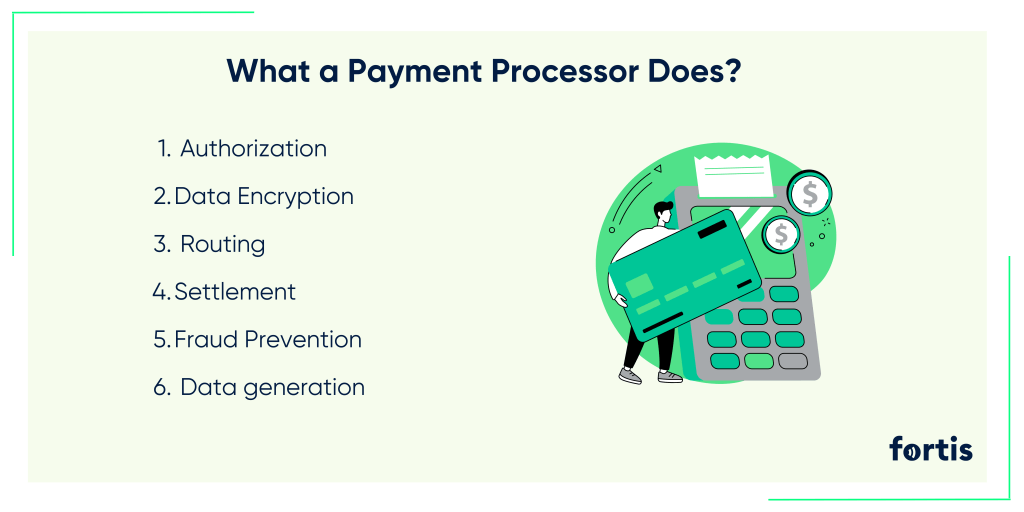

What a Payment Processor Does?

A payment processor performs several crucial tasks to ensure the smooth handling of your transactions:

- Authorization: When a customer makes a payment, the processor verifies whether the customery has sufficient funds or credit to complete the transaction.

- Data Encryption: To protect sensitive payment information, the processor encrypts the data, safeguarding it from potential security breaches.

- Routing: The processor sends transaction details to the relevant card network (Visa, Mastercard, etc.) and the customer’s issuing bank.

- Settlement: Once the transaction is approved, the processor ensures the funds are transferred from the customer’s account to your business account.

- Fraud Prevention: Advanced processors use AI and machine learning to detect and prevent fraudulent activities, offering peace of mind for both you and your customers.

- Generates data: Payment processors generate valuable data on customer transactions, which can be used to create detailed reports, analyze sales trends, and gain insights into business performance. You can leverage this information to make informed decisions and optimize your operations.

How Does a Payment Processor Work?

1. Customer Initiates Payment: Customer initiates the payment process by entering their payment information

- Online: The customer selects items, proceeds to checkout, and enters their payment information (credit card number, expiration date, CVV, etc.) on your website or through a payment link.

- In-Person: The customer swipes, dips, or taps their card at a point-of-sale (POS) terminal.

2. Payment Gateway:

- The merchant's website or POS terminal sends the payment information to a payment gateway.

- The payment gateway encrypts the sensitive data to protect it during transmission.

3. Payment Processor:

- The payment gateway forwards the encrypted information to the payment processor. Payment processors use strong encryption algorithms like AES to secure sensitive data during transmission and storage.

- The processor decrypts the data and validates the information, such as card number, expiration date, and CVV. Instead of storing actual card numbers, payment processors often replace them with unique tokens, which reduces the risk of data breaches.

- The processor then sends a request to the card network (Visa, Mastercard, American Express, etc.) for authorization.

4. Card Network:

- The card network routes the authorization request to the issuing bank (the customer's bank).

- The issuing bank verifies the customer's account balance or credit limit to determine if the transaction can be approved.

5. Authorization Response:

- The issuing bank sends an authorization response to the card network, which then forwards it to the payment processor.

- The processor receives the response and notifies the merchant whether the transaction is approved or declined.

6. Transaction Settlement:

- If the transaction is approved, the processor sends a settlement request to the acquiring bank (the merchant's bank).

- The acquiring bank transfers the funds to the merchant's account, minus any processing fees.

- The settlement process typically takes a few business days.

Key Features of Payment Processors

Modern payment processors offer a range of features to improve efficiency and enhance customer experiences:

- Multi-Currency Support: Essential for businesses serving international customers.

- Recurring Billing: Perfect for subscription-based models.

- Mobile Payments: Enables customers to pay via mobile wallets like Apple Pay or Google Pay.

- Analytics and Reporting: Provides insights into sales trends and transaction data.

- Fraud Detection: AI-powered tools to identify and block suspicious transactions.

Payment Processor Merchant Services

Merchant services are the additional tools and support services provided by payment processors. These can include:

- Chargeback Management: Handling disputes with customers and card issuers.

- POS Hardware: Physical terminals for card payments in-store.

- Payment Gateways: Online portals for e-commerce transactions.

For UAE-based businesses, merchant payment processors like Fortis offer end-to-end solutions that simplify payment management and improve operational efficiency.

How to Choose the Right One for Your Business

If you are a small business operating in the UAE, then there are several factors you need to consider before making a decision such as:

Business Model and Needs

Your choice of a payment processor depends significantly on the type of business you run. If you’re operating an e-commerce platform, prioritize a processor with robust payment gateway integration to. This ensures that online transactions are smooth, secure, and compatible with popular shopping platforms like Shopify or WooCommerce. Features such as support for multiple currencies, seamless checkout processes, and mobile optimization are crucial for enhancing the customer experience.

For physical stores, the focus shifts to reliable Point-of-Sale (POS) systems. These systems should include features like card readers, receipt printing, and compatibility with contactless payment options like Apple Pay or Google Pay. If you have a hybrid business model—combining in-store and online sales—look for a payment processor that supports both environments under one platform.

Transaction Volume

Your business’s transaction volume plays a critical role in determining the cost-effectiveness of a payment processor. High-volume businesses often benefit from processors offering tiered or custom pricing models. These pricing structures reduce per-transaction fees as your volume increases, making them more economical over time.

Conversely, if your business processes a lower volume of transactions, a processor with flat-rate pricing might be more suitable, ensuring predictable costs. Always consider the total cost of ownership, including setup fees, monthly charges, and additional fees for chargebacks or refunds, as these can vary widely between providers.

Security Features

Security is a non-negotiable aspect of payment processing. A reliable payment processor should comply with the Payment Card Industry Data Security Standard (PCI DSS), which sets the benchmark for secure transactions.

Tokenization is another essential feature to look for—it replaces sensitive card details with a unique token, ensuring that customer data remains secure even if a breach occurs. Fraud detection and prevention tools, powered by AI and machine learning, help identify suspicious activities in real time, adding an extra layer of protection for your business and customers. End-to-end encryption is also crucial to safeguard data from the point of entry to its final destination.

Integration

Seamless integration with your existing systems is key to running an efficient business. If you’re an e-commerce business, your payment processor should integrate effortlessly with your platform, enabling features like automated payment processing, order tracking, and inventory updates.

For physical stores, integration with your accounting software and inventory management systems ensures accurate financial reporting and inventory tracking. Some payment processors also integrate with customer relationship management (CRM) tools, helping you gain insights into customer behavior and improve engagement strategies. The more integrated your systems, the less manual work required, allowing you to focus on growth.

Customer Support

Even with the best payment processor, issues can arise—whether it’s a failed transaction, a technical glitch, or a question about fees. That’s why responsive and reliable customer support is crucial. Look for a provider that offers 24/7 support through multiple channels, including phone, email, and live chat.

Customer support quality can be a make-or-break factor, especially for small businesses that lack in-house technical expertise. A processor with a dedicated support team ensures that problems are resolved quickly, minimizing downtime and maintaining a smooth customer experience. Some providers also offer resources like FAQs, tutorials, and setup guides to help you navigate their systems independently.

By carefully evaluating these factors, you can select a payment processor that aligns with your business model, scales with your growth, and provides the reliability and security you need to succeed.

Conclusion

Choosing the right payment processor is a crucial decision for your business. Whether you’re looking for the best payment processor for online businesses or an all-in-one solution for both e-commerce and physical sales, understanding your needs and evaluating key features will help you make the best choice.

.png)