.svg)

.svg)

.jpeg)

[[highlight_1]]

According to Mastercard's SME Confidence Index, 92% of small and medium-sized businesses in the UAE now accept digital payments and many have dropped cash altogether, which means choosing the right payment gateway in UAE has never mattered more. For SMEs, more options means more decisions. However, the wrong gateway can cost you in fees, settlement delays, or a checkout experience that loses customers before they pay.

This guide covers the top 10 payment gateway options for UAE SMEs in 2026 and a straightforward recommendation for every business type.

What is a Payment Gateway?

Think of it as the invisible step between a customer tapping their card and the money appearing in your account. The gateway checks the card, asks the bank for approval, gets a yes or no, and logs the sale, all before the receipt prints. You never see it working, but without it, nothing moves.

Payment Gateway vs Payment Processor vs Acquirer

These terms are often used interchangeably, but they mean different things, and the difference matters when you are comparing costs and choosing the right online payment solution for small business Dubai.

Most UAE SMEs use a gateway that bundles the gateway and processor roles together. The acquirer is typically your UAE bank.

What to Look for Before You Decide

Before you start comparing providers, these eight questions are worth answering first:

Transaction fees (MDR):

A blended rate of 2.5%–3.0% per transaction is typical for UAE SMEs on domestic cards. Rates above 3.5% warrant a closer look.

AED vs USD settlement:

Some international gateways settle in USD, which adds a conversion cost. AED settlement is preferable for local businesses.

Local bank compatibility:

UAE transactions require 3D Secure (OTP verification). Confirm the gateway supports this flow with local bank issuers.

Supported payment methods:

Check for Visa, Mastercard, Apple Pay, Google Pay, Tabby, Tamara, and Jaywan coverage.

Setup requirements:

Most UAE gateways require a trade licence, corporate bank account, VAT certificate, and a working website URL. Some accept payment links as a substitute for a website.

Buy Now Pay Later (BNPL) support:

For retail and e-commerce businesses, offering Tabby or Tamara at checkout can increase average order value significantly. Check whether your gateway supports native BNPL integration before signing up.

Reliability and uptime:

When a customer is ready to pay, even a few seconds of downtime can cost you a sale. Prioritise gateways with a proven track record of 24/7 availability and responsive technical support.

Global reach:

If your customers include tourists, expatriates, or international buyers, confirm the gateway supports cross-border payments and multi-currency acceptance in their home markets. Not all UAE-licensed gateways are optimised for outbound international transactions.

Top 10 Payment Gateways in UAE for SMEs (2026)

Pricing marked with * is based on industry sources, not the provider's own published rates. Use it as a starting point, not a final number.

1. Network International (N-Genius): Best for Enterprise and Multi-Location Merchants

Network International is the payment infrastructure that most UAE businesses run on whether they know it or not. Their N-Genius platform covers both online and in-store payments under one account, which makes it a natural fit for businesses that want a single provider for everything.

Pricing: MDR typically ranges from 1.5% to 3.5% depending on business category and volume. Pricing is negotiated directly.

Best for:

Multi-location retailers, hospitality groups, all kinds of SMEs

Key features:

End-to-end acquiring and gateway, UAE Central Bank compliant, combined in-store POS and online gateway

Watch out for:

Not a self-service setup.

Don’t have a website? Send a payment link to your customers and accept payments online.

2. Telr: Best for UAE E-Commerce and Startups

Telr is a UAE-founded gateway with strong local bank integrations. Every plan comes with the same full feature set, and there is no setup fee.

VAT at 5% applies to all fees.

Best for:

UAE e-commerce stores, startups, subscription businesses, social commerce

Key features:

120+ currencies, Tabby BNPL, Shopify/WooCommerce/Magento plugins, payment links and QR codes via Telr Social

Watch out for:

The Entry plan suits businesses processing up to AED 20,000/month. Below that threshold, evaluate whether the fixed monthly fee is justified by your transaction volume.

3. PayTabs: Best for MENA-Wide and B2B Businesses

PayTabs is built for businesses that sell across multiple countries or need to route payments at an enterprise level. If you run a marketplace, manage B2B invoicing, or operate in several MENA markets at once, it is one of the few gateways in the region that handles this well.

Industry-reported. Monthly fee quoted in USD by some sources, verify current AED equivalent at paytabs.com.

Best for:

Multi-country sellers, B2B invoicing, marketplace businesses

Key features:

100+ payment methods, ML-based fraud detection, API-first integration, split payments

Watch out for:

Monthly fee in USD adds a conversion cost for AED-based SMEs

4. Stripe: Best for Developer-Led and SaaS Businesses

Stripe has no monthly fee, no setup cost, and an API that most developers already know. It works in the UAE and supports AED transactions, though funds settle in USD by default.

Pricing: 2.9% + AED 1 per transaction. No monthly fee. International card surcharge and currency conversion each add 1.5%.

Best for:

Tech startups, SaaS businesses, globally-facing UAE companies

Key features:

Extensive API library, Stripe Radar fraud detection, Apple Pay and Google Pay, recurring billing

Watch out for:

USD default settlement adds a conversion step for AED-focused businesses

5. Amazon Payment Services: Best for Retail E-Commerce

Formerly Payfort, Amazon Payment Services runs the payments infrastructure behind Amazon.ae. For retail businesses, the brand recognition alone tends to increase checkout confidence, and its GCC payment method coverage is hard to match.

Pricing: The Standard Plan is reported at AED 200/month with a transaction fee of 2.80% + AED 1 for monthly volumes under AED 300,000. Verify current rates directly at paymentservices.amazon.com.*

Best for:

Retail e-commerce, UAE marketplace sellers, businesses with GCC customers

Key features:

Tokenisation for returning customers, Mada, KNET, and Meeza support, installment options

Watch out for:

Requires technical integration and a direct quote for pricing

6.Checkout.com: Best for Scale-Up Businesses

Checkout.com is built for businesses that have outgrown standard gateway setups and need smarter routing, deeper analytics, and global scale. The pricing model rewards volume, so the more you process, the better your rates tend to be.

Pricing: Not publicly listed. Transaction fees are reported to start lower than most competitors at high volumes.*

Best for:

High-growth businesses, fintech companies, internationally-facing UAE businesses

Key features:

Intelligent routing to improve acceptance rates, 200+ countries, strong analytics dashboard

Watch out for:

Not cost-effective for low-volume SMEs. Requires developer resources.

7. Tap Payments: Best for GCC-First Businesses

Tap Payments is designed for the Gulf market, with native support for local payment methods across UAE, Saudi Arabia, Kuwait, Bahrain, and Qatar, including a bilingual Arabic/English checkout experience.

Pricing: Industry-reported averages in the 2.37%–2.6% range for payment link and QR transactions. Card-present rates vary.* Verify at tap.company.

Best for:

Businesses with a Gulf-wide customer base, Arabic-language checkout requirements

Key features:

GCC local payment method coverage, payment links and QR payments, bilingual checkout

Watch out for:

Less globally recognised than Stripe or Checkout.com

8. Magnati: Best for FAB Banking Customers

Magnati was spun out of First Abu Dhabi Bank (FAB) and operates as a UAE-regulated acquirer and gateway in one. If your business banks with FAB or operates in a government-adjacent sector, the integration is more straightforward than most alternatives.

Pricing: MDR typically in the 1.8%–3.8% range depending on business category and volume. Negotiated directly.*

Best for:

FAB banking customers, government-adjacent businesses, enterprise merchants

Key features:

UAE Central Bank regulated, Jaywan support, combined in-store and online coverage

Watch out for:

Not widely known outside FAB-connected businesses. Not a self-service setup.

9. Ziina: Best for Freelancers and Micro-Businesses

Ziina was built for people who just want to get paid without setting anything up. You share a link or a phone number, the customer pays, and the money moves. That is more or less all there is to it.

Pricing: No monthly fee. Transaction fees reported at approximately 2.5%–3.5% for business accounts.* Verify at ziina.com.

Best for:

Freelancers, micro-businesses, very early-stage setups

Key features:

Payment via phone number or link, no integration needed, Arabic support

Watch out for:

Limited reporting tools and no deep e-commerce integrations

Comparison Table

Settlement periods are approximate and may vary by account type and bank.

Also Worth Knowing: Adyen, PayPal, TotalPay, and PayDo in UAE

These four names come up regularly in UAE payment gateway research. None made the top 10 for SMEs, but each has a specific context where it makes sense.

Adyen

Adyen is one of the most capable payment platforms available globally, used by companies such as Uber, Spotify, and McDonald's. It supports online, in-app, and in-store transactions from a single platform with advanced analytics and routing. In the UAE, it serves larger enterprises and regional chains. For most SMEs, the entry requirements and minimum volumes put it out of reach at an early stage. Worth revisiting when your monthly volumes justify enterprise-level pricing.

PayPal

PayPal is widely recognised by international customers and can add a layer of buyer trust for businesses with a global audience. That said, transaction fees for international payments run above 4%, and withdrawing funds to a UAE bank account is more complicated than it sounds. If most of your customers are in UAE or the GCC, a local gateway is simpler and cheaper.

TotalPay

TotalPay is a UAE-founded gateway established in 2022, built primarily for local SMEs and mid-sized businesses. It supports 200+ payment methods, QR payments, mobile wallets, and PCI-DSS compliance, with a performance dashboard included.

Shopify integration is not natively supported, which limits its fit for standard e-commerce setups. Settlement timelines are not publicly disclosed. Worth monitoring as it continues to grow its local presence.

PayDo

PayDo is a UK-founded gateway that serves cross-border merchants and businesses in high-risk or niche industries that mainstream UAE gateways may decline. It supports 24 currencies including AED, requires no reserve account, integrates 350+ payment methods, and offers fast settlement to PayDo accounts.

It is not a first-choice gateway for standard UAE retail or F&B SMEs, but it fills a genuine gap for digital product sellers, subscription businesses, or merchants with international-first revenue.

How to Accept Online Payments in UAE: What You Will Need

Before a UAE payment gateway approves your merchant account, you will typically need to provide:

- Valid UAE Trade Licence

- UAE corporate bank account

- VAT Registration Certificate (if applicable)

- Working website URL, or a confirmed payment link model where accepted

- KYC documentation for the business owner

Approval timelines vary. Self-service gateways like Telr and Stripe typically activate within one to three business days. Bank-linked gateways such as Network International and Magnati take longer due to additional due diligence.

When a POS System Makes More Sense Than a Payment Gateway

Most of the gateways covered in this guide are built to solve one problem: processing payments online. However, if your business also runs pop-ups or participates in events, a standalone payment gateway addresses only a fraction of what you actually need to run your business day to day.

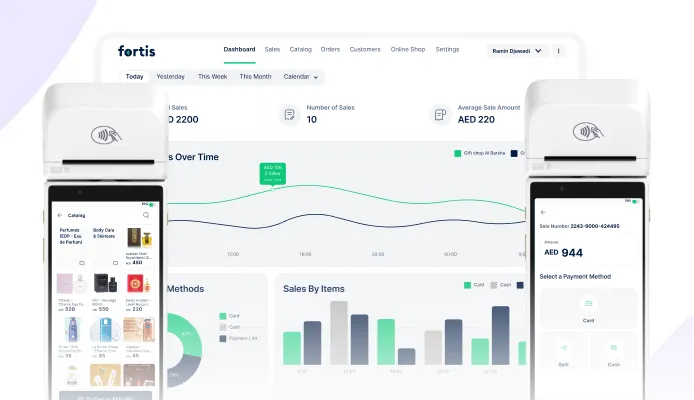

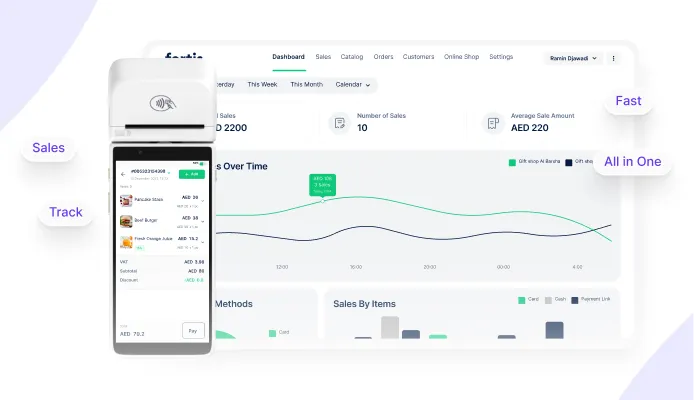

Fortis SmartPOS is built differently. It converts a standard card machine into a complete point-of-sale system that you can carry anywhere. Moreover, you can use Fortis SmartPOS to convert

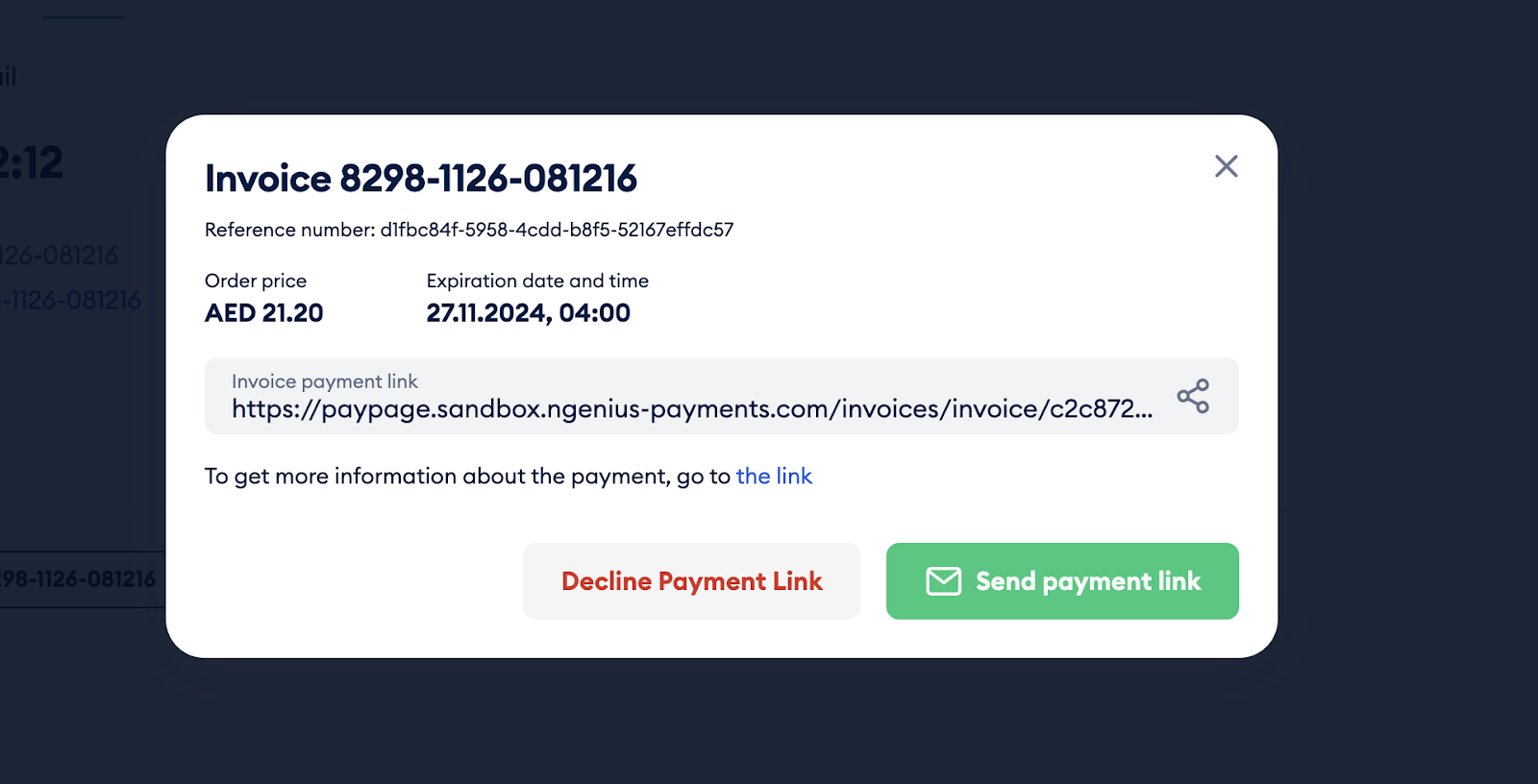

Plus, payment links are included within Fortis SmartPOS, which means you can also accept payments remotely via WhatsApp or any messaging channel. As a pop-up, a food truck, or a service business that invoices clients outside of the counter, this removes the need to pay for an additional tool.

FAQ

What is MDR in UAE payments?

MDR stands for Merchant Discount Rate, the percentage fee a merchant pays per card transaction. In the UAE, MDR typically ranges from 1.5% to 3.5% for domestic transactions depending on the gateway, card type, and business category. It is the primary cost metric to compare across providers.

Can I accept online payments in the UAE without a website?

Yes. Options that do not require a website include Telr Social, Ziina, Tap Payments, and Fortis Payment Links. Which one fits depends on whether you need payment collection as a standalone tool or as part of a wider merchant system that handles reporting, loyalty, and inventory.

What is the cheapest payment gateway in the UAE?

For businesses with no monthly fee requirement, Stripe and Ziina charge only per transaction. For higher volumes, Telr's Medium plan at AED 99/month with a 2.49% transaction fee offers the best combination of low cost and publicly verified pricing in its category.

Is Stripe available in the UAE?

Yes. Stripe supports UAE businesses and AED transactions. Settlement defaults to USD, which adds a conversion step. It is best suited for tech-forward businesses with developer resources rather than traditional retail or service SMEs.

What is the difference between a payment gateway and a POS system?

A payment gateway processes online payments through a website or app. A POS system manages in-store payments, inventory, orders, and sales data at the point of sale. Some providers, including Network International and Fortis, combine both in a single ecosystem.

Go Online With Fortis

As a small business, it is sometimes difficult to spare the time and budget to set up a website and take your business online. However, in a market like the UAE, it is extremely important to have an online presence.

With Fortis, you can go online without the hassle of setting up a website. Here is how:

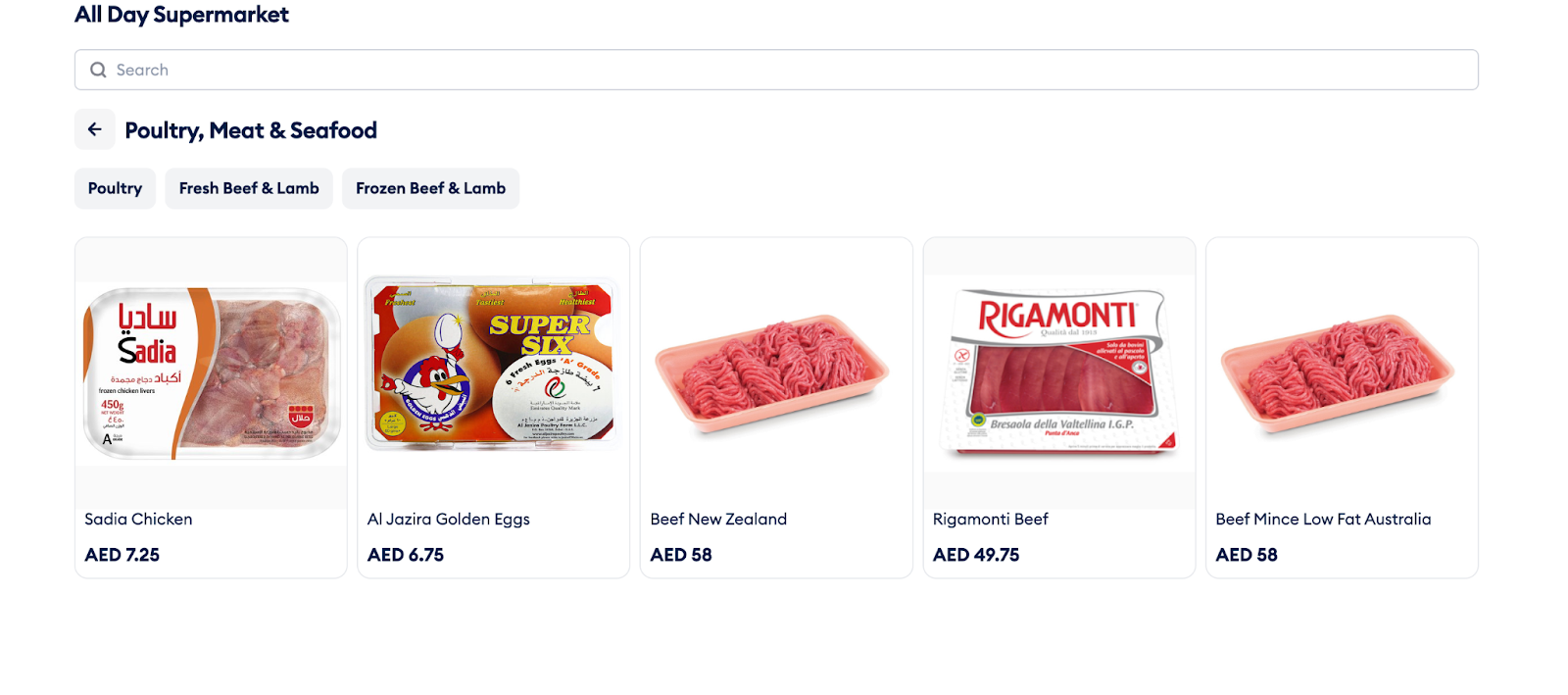

Online Catalog

With Fortis POS solution, you can convert your catalog into an online store with just one click without any training, or expertise. You can share this catalog with your customers or even use it in social media campaigns.

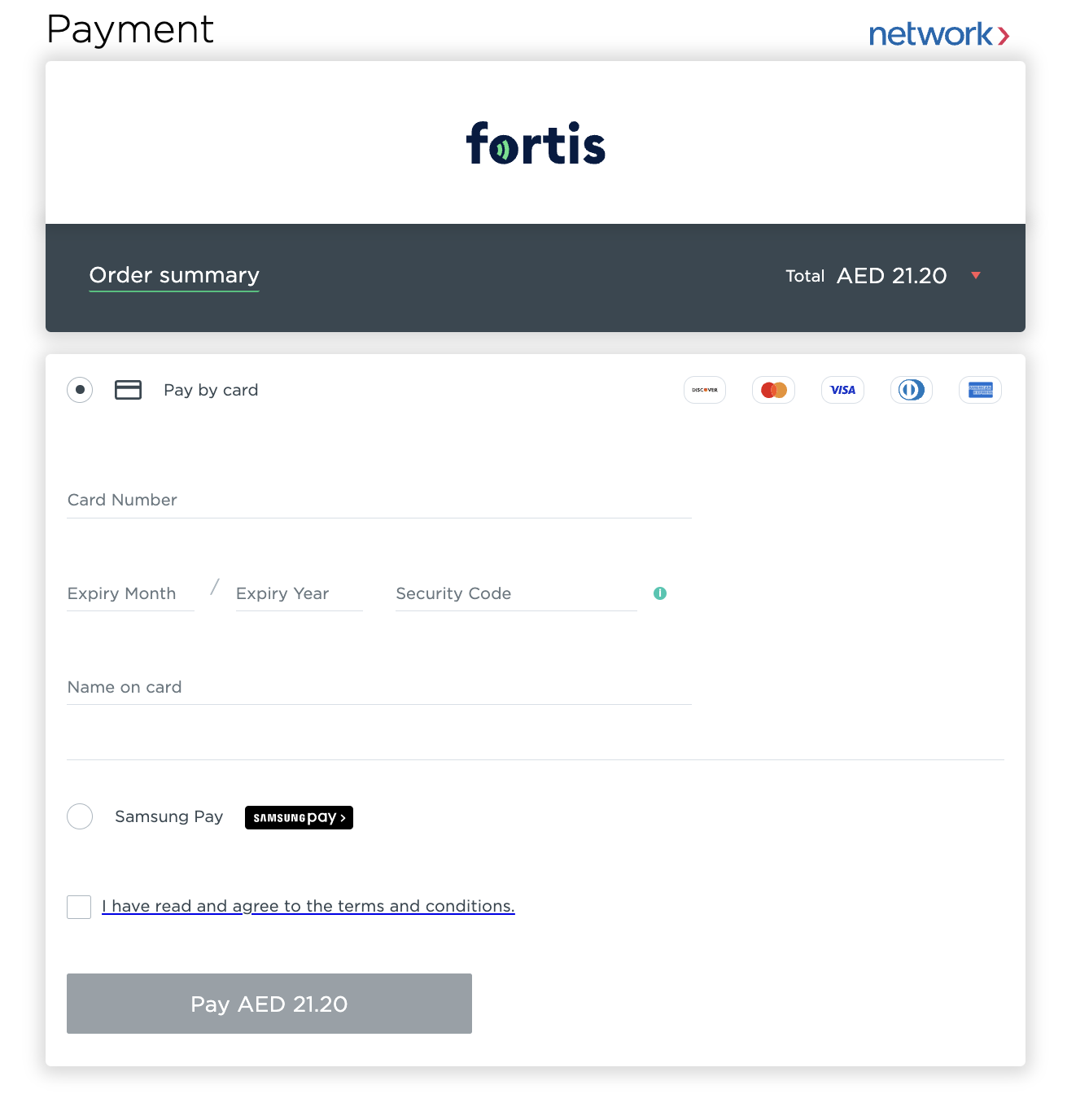

Customers can select items and add them to the cart. Once they are ready to pay, the online catalog redirects them to the checkout page or payment gateway hosted by Fortis in collaboration with Network International. Customers can then choose to pay by credit card, debit card, Samsung Pay and even Apple Pay.

Payment Links

If you sell through social media such as instagram or Facebook for example, you can also create an order in the Fortis POS solution and then send a payment link to your customers. Once customers click on the link, it redirects them to the payment gateway where they can pay through card, or Samsung or Apple Pay.

Conclusion

Payment gateways are the foundation of online payments and ensure your customers can pay securely and conveniently. Whether you're just starting your online journey or scaling to new markets, an efficient and reliable payment gateway is essential for success.

If you are a small business that wants to go online, then you can do so with Fortis POS solution. Book a demo today and go online without any extensive investment.