.svg)

.svg)

[[shortcode1 title="Quick Answer:" description="Credit card processing in the UAE refers to the system that allows businesses to accept card payments from customers. It involves your POS terminal or card machine, a payment service provider (such as Network International), the customer’s issuing bank, and the card network (Visa or Mastercard). To start accepting card payments, you need a valid trade license, a UAE business bank account, and a merchant account with a payment service provider."]]

Regardless of the business you are operating in the UAE, card payments are no longer optional. Customers expect to tap and pay, whether they are grabbing a morning coffee in JLT or picking up skincare products at a mall kiosk. Customers expect to tap and pay, whether they are grabbing a morning coffee in JLT or picking up skincare products at a mall kiosk." That sentence is currently just an assertion; this stat gives it real backing. Something like:

Visa's latest research shows 68% of UAE consumers are now largely non-cash users, up from 61% the year before, making most of their everyday payments by card or mobile device.

And while accepting cards sounds straightforward, the mechanics behind it, fees, settlement timelines, VAT compliance, and reconciliation, affect how smoothly your business actually runs day to day.

This guide explains how credit card processing works in the UAE, what it costs, and how to choose a setup that fits your operations, not just your budget.

What Is Credit Card Processing in the UAE?

Credit card processing is the infrastructure that moves money from your customer's bank to yours every time they pay by card. It sounds instant, but there are several parties involved, each playing a specific role.

Here is the core flow:

- Customer initiates payment by tapping or inserting their card at your terminal

- Your card machine or POS sends the transaction details to your acquiring bank (Mashreq, Emirates NBD, or ADCB)

- The acquiring bank routes the request through the relevant card network, such as Visa or Mastercard, depending on the card used and the provider’s supported networks.

- The card network contacts the customer's issuing bank to verify funds and approve or decline

- Approval is sent back through the same chain to your terminal in seconds

- Settlement happens later, usually within one to three business days, when funds land in your account minus processing fees

Understanding this flow matters because your choice of acquiring bank affects your fees, settlement speed, and the level of support you get when something goes wrong. If you want a deeper understanding of the companies and technology providers involved in processing transactions behind the scenes, read our guide on payment processors in the UAE.

Who's Involved in Credit Card Processing?

Every card payment you accept passes through several parties before the money lands in your account. Knowing who does what helps you understand your fees, your settlement timelines, and who to call when something goes wrong.

Cardholder

The customer pays with their debit or credit card, whether tapping, inserting, or paying online.

Merchant

That's you. You accept the payment through your card machine, POS terminal, or online checkout.

Acquiring bank

The bank that gives you a merchant account and settles funds into your business account after a sale. Network International, Mashreq, Emirates NBD, and ADCB are among the acquiring banks operating in the UAE.

Issuing bank

The customer's own bank, the one that issued their card. It checks whether the customer has sufficient funds and approves or declines the transaction.

Card network

The rail the transaction travels on, such as Visa or Mastercard. The network sets the rules and connects the acquiring bank to the issuing bank.

Payment processor

The technology layer that handles the transaction data behind the scenes, passing information between your POS, the acquiring bank, and the card network.

Payment gateway

Relevant mainly for online payments, the gateway encrypts and transmits card details from a checkout page to the payment processor. If you only accept in-person payments through a card machine, you won't need one.

You don't need to manage most of these relationships directly. Your acquiring bank and your POS provider handle the connections. What matters for you is choosing an acquiring bank with fair fees and reliable settlement, and a POS system that ties the payment data back into your sales and VAT records automatically. If you want to go deeper on how processors and gateways differ, especially if you're planning to sell online as well as in person, read our breakdown of payment processors vs. payment gateways.

How Credit Card Payments Actually Work for UAE Businesses

A customer orders a specialty coffee at your Dubai café and pays AED 28 using a Visa card. Here is what happens behind the scenes:

- Your payment terminal captures the card details and sends an authorization request.

- The card network (Visa or Mastercard) routes the request to the customer’s issuing bank.

- The bank checks available funds and either approves or declines the transaction within 1–3 seconds.

- The approval is sent back to your terminal, and the sale is recorded in your POS system.

- At the end of the day, the transaction is included in the settlement process.

- Within 1–3 business days, the funds (AED 28 minus the MDR fee) are deposited into your business account.

This process is consistent whether you are running a specialty café in Dubai, a perfume pop-up in City Walk, a padel court membership desk, or a multi-branch restaurant across Abu Dhabi and Dubai.

What changes is not the core payment flow, but the fee structure, settlement terms, and how well your POS system helps you track sales, reconcile transactions, and manage financial reporting.

What Small Businesses Need Before Accepting Card Payments

Before your first card tap, you need a few things in place:

Trade License

Your business must be legally registered in the UAE. This applies whether you are a mainland LLC or a free zone company. Without a valid trade license, acquiring banks will not open a merchant account for you.

UAE Business Bank Account

You will need a corporate or business account, not a personal one. This is where settlements land after card transactions are processed. Most acquiring providers require a business bank account before they can activate card payment services for your business.

Merchant Account with an Acquiring Bank

Network International, Magnati, Mashreq, Emirates NBD, and First Abu Dhabi Bank are among the main acquiring and payment providers operating in the UAE. Each provider has different onboarding requirements, fee structures, terminal options, settlement timelines, and support models.

A Card Machine or POS Terminal

You can either get a basic payment terminal or a full SmartPOS system, depending on your operational needs. A basic terminal accepts payments. A SmartPOS system handles payments, inventory, sales reporting, VAT invoices, and customer data from one device.

VAT Registration (If Applicable)

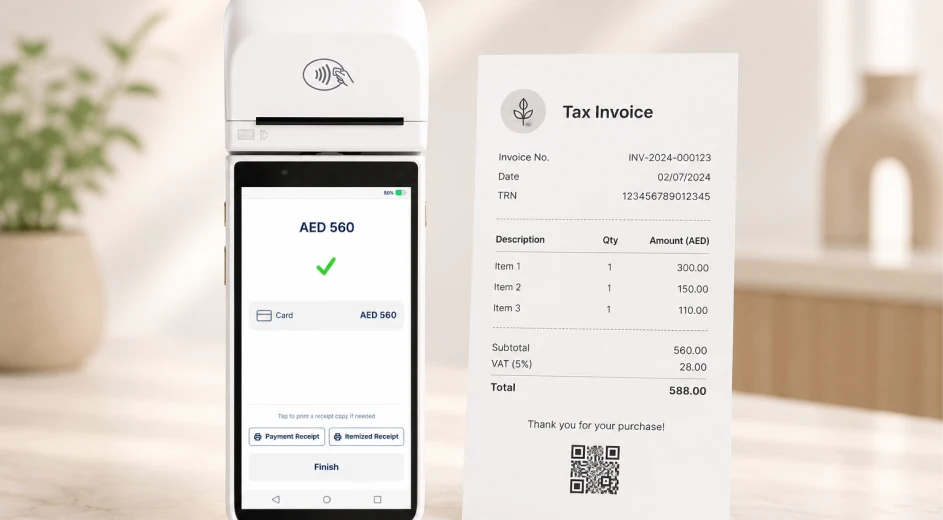

If your annual taxable revenue exceeds AED 375,000, you are required to register for VAT with the Federal Tax Authority. If you are VAT-registered, your business must issue FTA-compliant tax invoices, not just payment receipts. These invoices should include the required tax details, such as your TRN, invoice date, taxable amount, VAT amount, and total payable amount, according to Federal Tax Authority requirements.

Understanding Credit Card Processing Fees in the UAE

Fees are where most small business owners get surprised. Here is what you are actually paying for:

Merchant Discount Rate (MDR)

The MDR is the core processing fee charged as a percentage of each transaction. For many UAE SMEs, MDR can vary widely depending on the acquiring bank, transaction volume, card type, business category, and whether the card is local or international.

As a practical benchmark, small businesses may see rates around 1.5% to 3.5%, but the final rate should always be confirmed with the acquiring provider.

The main factors that affect your MDR include:

- Your acquiring bank

- The card type, such as local Visa debit vs. international premium Mastercard

- Your business category and monthly transaction volume

- Whether the card is present or not, such as in-person vs. online payments

On an AED 500 retail sale with a 2% MDR, you receive AED 490 before considering any other fees. On high-volume days, that difference can add up quickly.

For many SMEs, the processing fee is only part of the total cost of accepting card payments. Businesses also spend time reconciling transactions, preparing VAT records, and combining reports from multiple systems. As transaction volumes grow, operational efficiency becomes just as important as the processing rate itself.

Terminal and Hardware Costs

If you are renting a card machine from your acquiring bank, expect a monthly rental fee. If you own your terminal, there is no rental, but you may pay for support, maintenance, or upgrade costs depending on your provider.

Software and POS Subscription Fees

A basic card machine may not require a separate POS software subscription, although rental, support, or service fees may still apply depending on the provider. A SmartPOS platform that adds sales dashboards, inventory management, and loyalty comes with a software subscription. Most UAE SMEs find this more cost-effective than buying standalone tools for reporting, invoicing, and customer management separately.

Who Pays the 3% Credit Card Fee?

This is a common question. In most UAE retail and service businesses, the business absorbs card processing fees as part of its operating costs, similar to expenses such as packaging, utilities, or software subscriptions.

If you are considering adding a visible card surcharge, first check your acquiring provider’s terms and the applicable card scheme rules. In many cases, surcharging card payments may be restricted by Visa, Mastercard, or your acquirer agreement, and could create both compliance and customer-experience issues.

Some businesses build processing costs into their pricing structure. Others negotiate lower MDR rates with their acquiring provider once they reach consistent monthly transaction volumes.

Traditional Card Machines vs. SmartPOS Systems

Most UAE SMEs start with a basic card machine from their bank. It works, but its primary purpose is to process payments.

The practical difference shows up in day-to-day operations. A salon running only a card machine may still need to manually review terminal transactions, reconcile deposits, track cash payments separately, and prepare VAT records from multiple sources. This process can create significant administrative work at the end of each day.

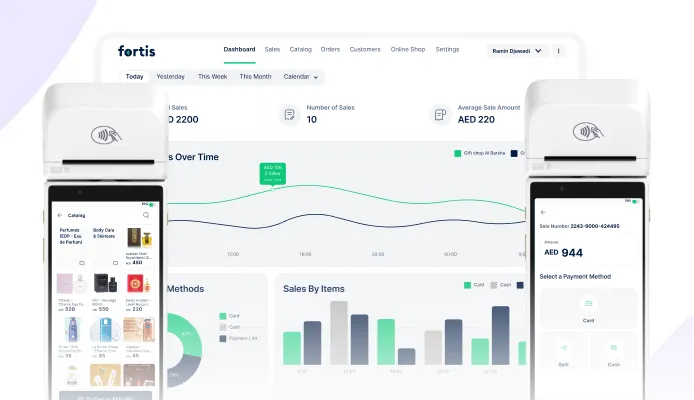

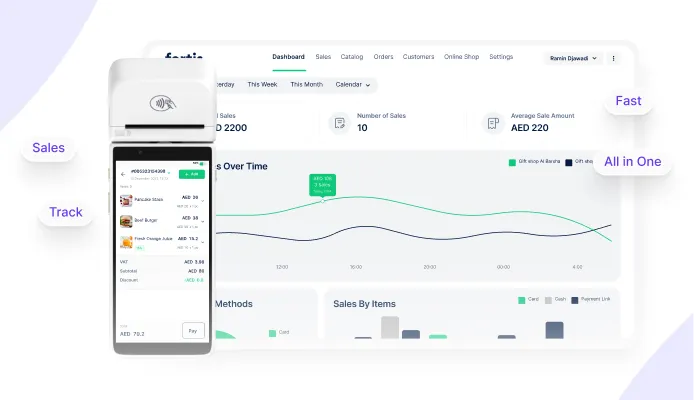

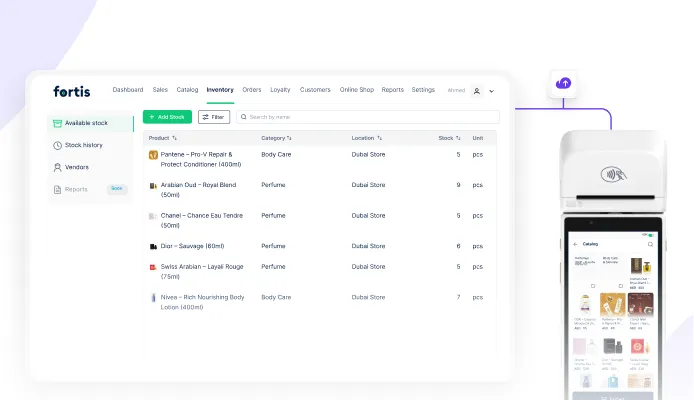

A salon running Fortis SmartPOS has a live dashboard showing sales by payment method, and service category. VAT records are generated automatically, and inventory updates in real time as products are sold.

The biggest difference is often operational rather than transactional. Businesses gain better visibility, reporting, and reconciliation without relying on multiple disconnected systems.

Why Restaurants and Cafes in the UAE Are Moving Toward Integrated Payments

For food and beverage businesses, payment is not just a transaction. It is a touchpoint that affects table turnover, staff workload, customer experience, and online reputation.

The traditional flow is slow. A customer finishes their meal, asks for the bill, waits for the waiter, reviews the paper check, pays by card, waits for the handheld terminal, then waits again for the receipt. In a busy café, those extra minutes can delay the next table.

For restaurants, credit card processing is not only about accepting the payment. It is also about how quickly the customer can review the bill, split it, tip, and complete payment without slowing down the table.

For many restaurants, improving payment processing is not only about accepting cards. It is also about reducing wait times and making the payment experience more convenient for guests.

Fortis Table Pay adds this payment experience layer through a QR code on the table. A customer scans it, sees the itemised bill, splits it by item or number of people, adds a tip, pays by card or Apple Pay/Google Pay, and can leave a Google review from their phone. No waiting. No extra staff movement.

For restaurant owners, this means:

- Faster table turnover during peak hours

- Tips collected digitally with accurate records

- Guests can be prompted to leave a Google review after payment

- Integration with Foodics and Syrve for full POS syncing

Common Credit Card Processing Mistakes UAE SMEs Make

Choosing the cheapest acquiring option only: A lower MDR sounds better until you realize the provider has slow settlement timelines, poor support, or terminal compatibility issues with your POS software.

Not reconciling card and cash separately: Many small business owners combine cash and card transactions into a single daily total. When discrepancies appear, they become much harder to trace and resolve.

Issuing incomplete VAT documentation: If you are VAT-registered, relying solely on a payment receipt may not satisfy UAE VAT documentation requirements. Businesses should ensure they issue the appropriate tax invoice or tax documentation required under FTA rules.

Using fragmented systems: A standalone card machine plus a separate accounting app plus a manual spreadsheet for inventory creates multiple sources of data that never quite match.

No visibility across locations: A basic card machine gives you terminal-level data per branch. You may not have a consolidated view of sales performance across locations.

Missing the loyalty opportunity at checkout: A basic terminal lets the payment moment pass. An integrated POS can make it easier to capture customer information and enroll customers in a loyalty program at checkout.

Conclusion

Accepting card payments in the UAE is now a basic customer expectation. The real decision is whether your setup only processes payments, or also helps you manage reporting, reconciliation, VAT records, and customer data.

A basic card machine can complete the transaction. A connected POS setup gives you clearer visibility into how your business is performing every day.

If your current payment flow still relies on manual reporting, disconnected systems, and end-of-day reconciliation, Fortis SmartPOS can help bring payments and day-to-day operations into a single workflow.

FAQ

How do I start accepting credit card payments as a small business in the UAE?

You need a valid trade license, a UAE business bank account, and a merchant account with an acquirer such as Network International, Mashreq, or Emirates NBD. Once approved, you will receive a card terminal and can begin processing payments. Setup typically takes a few days to two weeks depending on the acquiring bank.

What are the requirements for opening a merchant account in the UAE?

Most acquiring banks require a valid UAE trade license, a corporate bank account, proof of business address, and Emirates ID for the account holder. If you are on an investor visa or recently set up a free zone company, you may also need to provide your company incorporation documents and a recent bank statement.

Who pays the credit card processing fee in the UAE?

The business typically pays the fee, with the MDR deducted before settlement. Visible card surcharges may be restricted by card scheme rules or your acquiring provider agreement, so check your provider’s terms before applying one.

What is a typical MDR for UAE businesses?

MDR rates in the UAE generally range from 1.5% to 3.5% per transaction. The exact rate depends on your acquiring bank, your monthly card volume, and the types of cards your customers use. Higher volumes often allow you to negotiate lower rates with your bank.

Do I need a separate POS system or is a card machine enough?

A basic card machine is enough to accept payments, but it gives you no reporting, no VAT-compliant invoices, and no inventory tracking. If your business is growing and you need operational visibility, an integrated SmartPOS system running on your existing card machine is a more practical solution.

Should I use a basic card machine or a SmartPOS for VAT invoices?

A basic card machine may only issue a payment receipt, while a SmartPOS can generate POS-level tax invoices with VAT details at checkout. If you are VAT-registered, this can reduce manual invoicing work and make daily reconciliation easier.