.svg)

.svg)

.jpeg)

[[shortcode1 title="Quick Answer:" description="A POS payment is a transaction completed at the point where a customer pays for goods or services. It happens in person, at a physical terminal, using a card, cash, or digital wallet. The terminal communicates with the customer's bank in real time to confirm the payment and release the funds. In the UAE, VAT-registered businesses are required to issue an FTA-compliant tax invoice for each sale."]]

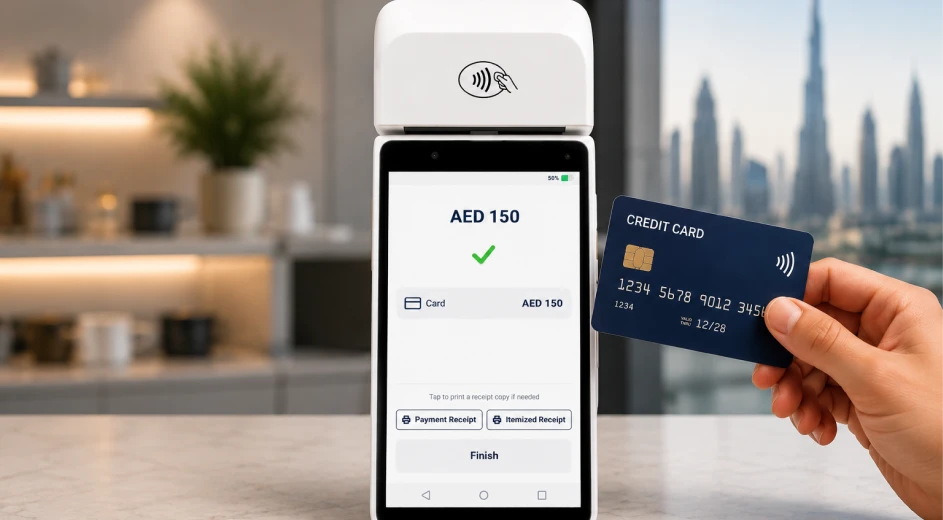

Picture a customer at the counter of your cafe in Dubai. They tap their phone on the terminal. Two seconds later, the payment goes through and a receipt is printed. That moment, simple as it looks, is a POS payment. It is also where most of the complexity in running a UAE small business begins.

For business owners in F&B, retail, and services, understanding how POS payments work, and what separates them from your wider POS system, directly affects how easily you can close your end-of-day reporting, how accurately you can calculate VAT, and how confidently you can grow.

What Is a POS Payment?

A POS payment, or point-of-sale payment, is the financial transaction that takes place when a customer pays for goods or services at the moment and location of purchase. It is the exchange of funds between the customer's bank and your business bank account, verified in real time through a payment terminal.

The "point of sale" is wherever that transaction happens: your checkout counter, the drive-through window, or a portable card machine at a pop-up stall.

POS payments are distinct from online payments, where the customer is not physically present. They are also distinct from the wider POS system, which we will cover in a dedicated section below.

How POS Payments Work

A POS payment completes in seconds, but there are several steps happening in the background. Here is the full flow:

- The customer presents their payment method: a card (chip & PIN or contactless), a digital wallet (Apple Pay or Google Pay), or cash.

- The terminal reads the card details via the chip, magnetic stripe, or NFC signal.

- The terminal sends an authorization request to the payment processor (the acquirer), which forwards it to the customer's card network: Visa, Mastercard, or another scheme.

- The card network routes the request to the customer's issuing bank.

- The issuing bank checks the account balance and fraud signals, then sends an approval or decline back through the same chain.

- The terminal receives the response and displays "Approved" or "Declined" in under two seconds.

- An FTA-compliant tax invoice is generated and either printed or sent digitally.

Cash payments follow a shorter path: the cashier records the amount, calculates change, and the sale is logged manually or through your POS system. In the UAE, you need to create receipts for cash transactions as well for VAT purposes.

Types of POS Payments

Not all POS payments work the same way. Here are the main types relevant to UAE businesses:

Chip and PIN

The customer inserts their card into the terminal and enters a four-digit PIN. This is the most common method for larger transactions where the bank requires identity verification.

Contactless (NFC)

The customer taps their card or phone on the terminal. Payment completes in under a second. In the UAE, contactless has become the standard for everyday transactions, driven by both customer preference and the Central Bank of UAE's push toward a cashless economy.

Digital Wallets

Apple Pay, Google Pay, and Samsung Pay all use NFC technology. The customer's card is tokenised on their device, so the actual card number never transmits. This adds a layer of security on top of the contactless flow.

Cash

Cash remains a POS payment, and in the UAE it must be handled correctly for VAT purposes. When a customer pays in cash, your terminal or POS system should still generate a simplified tax invoice with VAT itemised. Skipping this step creates compliance gaps.

QR and Mobile Payments

The customer scans a QR code displayed at the counter or on the table. Payment completes through their banking app.This method is increasingly used in UAE restaurants and cafes, especially in pay-at-table experiences where customers prefer not to wait for the bill.

POS Payment vs POS System: What Is the Difference?

One of the most common points of confusion for new business owners is treating these two terms as the same thing. They are not.

A POS payment is the transaction itself. A POS system is the full platform that manages your business around that transaction: your menu or product catalog, inventory, sales reports, customer data, VAT receipts, and staff tracking.

Here is how the two compare:

In practice, a business can have a POS payment without a POS system: your bank issues a card terminal that takes payments, and settlement data sits with the acquirer. But without a POS system layer, you have no sales history, no stock tracking, and no VAT receipts generated automatically. Most UAE SMEs need both.

POS Payment vs Online Payment

These two methods serve different customer journeys, use different technology, and carry different compliance requirements.

For UAE businesses that operate both a physical location and an online store, understanding this distinction matters for your VAT reporting. FTA rules treat in-person and online sales the same way for VAT purposes, but the receipt format and the way sales data flows into your accounting records can differ by system.

Why POS Payments Matter for UAE Businesses

Getting your payment flow right is not just about convenience. It directly affects three areas that determine how smoothly your business runs day to day.

Speed and Customer Experience

Long queues cost sales. A tap-to-pay terminal processes a transaction in under two seconds. For a busy cafe or retail outlet during peak hours, that speed is the difference between a smooth service and a bottleneck.

VAT Compliance

Every business registered for VAT in the UAE is required to issue an FTA-compliant tax invoice for each sale. The invoice must include your TRN, the VAT amount itemised at 5%, and the total payable. A POS system that generates this automatically on every transaction removes a significant compliance burden from your team.

Accurate Reporting

When your payments run through a terminal that does not talk to your POS software, your end-of-day close requires manual reconciliation. You are matching terminal settlement reports against POS sales records line by line. That process introduces errors and takes time that most small business owners do not have.

UAE-Specific Considerations for POS Payments

Terminals Issued by Banks and Acquirers

In the UAE, card terminals are typically issued by payment acquirers rather than sold directly to merchants. Network International is the dominant acquirer, providing terminals across thousands of UAE businesses. The terminal processes payments on behalf of your business, with settlement flowing into your business account.

The UAE Cashless Strategy

Dubai’s Cashless Strategy aims for 90% of all transactions in the emirate to be digital by 2026. For businesses operating in Dubai, this signals a clear shift toward card, wallet, and other digital payment methods. It also means customers will increasingly expect fast contactless payment options at checkout. Businesses that still rely heavily on cash-only workflows may find themselves less aligned with where the market is moving.

FTA Tax Invoices

The Federal Tax Authority requires all VAT-registered businesses to issue a tax invoice for every sale. For sales under AED 10,000, a simplified tax invoice is sufficient. This invoice must include the business name, TRN, date of supply, a description of goods or services, and the VAT amount. Your POS system should generate this automatically on every transaction, for both card and cash sales.

Common POS Payment Challenges

Reconciliation Gaps

When your card terminal and your POS software are separate systems, your settlement data and sales records live in two different places. At the end of day, you have to match them manually. Any discrepancy, a refund processed on the terminal but not in the POS, a split payment recorded differently across systems, requires investigation time.

Separate Systems, Double the Admin

A business running a bank-issued terminal alongside a separate POS tablet effectively manages two data streams. Customer data captured in the POS does not sync with the payment terminal. Sales reports have to be pulled from both systems and combined. This doubles the admin load and increases the margin for error.

Manual VAT Errors

If your terminal does not automatically calculate and itemise VAT on each sale, your team is doing it manually. For a busy service or retail outlet processing dozens of transactions a day, that is a consistent source of compliance risk.

How Modern POS Solutions Improve Payments

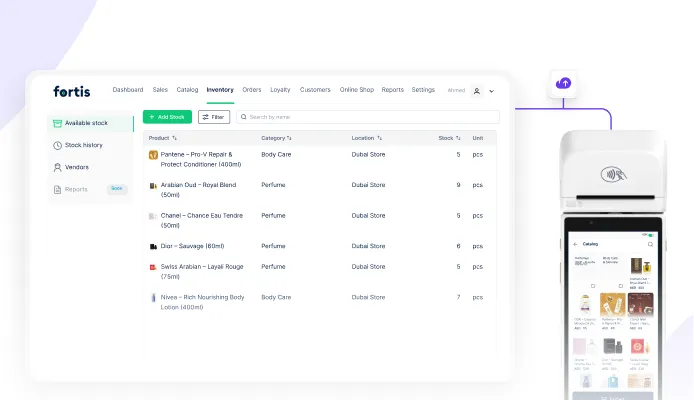

The most significant shift in how UAE SMEs handle payments in recent years is the move toward unified systems, where the POS software and the payment terminal are the same device.

Rather than running a POS tablet alongside a separate card machine, modern solutions convert the card machine itself into the POS. Orders, payments, customer data, and reporting all run from one device. The result is a cleaner operational flow and a much simpler end of day.

Fewer Devices, Less Reconciliation

When the POS and the payment terminal are the same device, sales and settlement data are always aligned. There is no manual matching at close, and no gap between what the POS recorded and what the bank settled.

Automatic VAT Compliance

A unified system generates FTA-compliant tax invoices on every transaction automatically, including cash sales, without your team having to think about it.

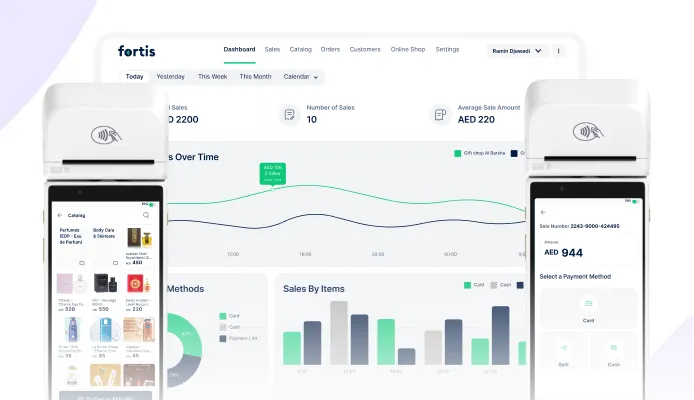

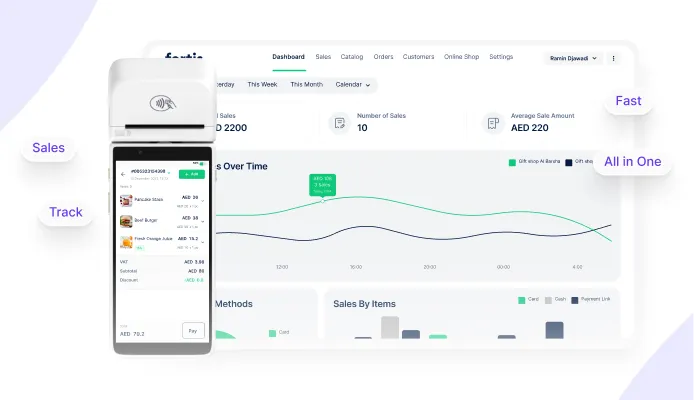

Real-Time Business Visibility

With POS and payments running together, your cloud dashboard reflects every sale as it happens. You can check your top-selling items, sales by staff member or location, and payment method breakdown from any device, without pulling reports from two systems.

Fortis SmartPOS takes this approach for UAE small and medium businesses. It converts your existing Network International card machine into a full POS system, so you can run payments, track sales, manage your catalog, and capture customer data from one device, without requiring new POS hardware in most cases. Sales sync to the Fortis merchant dashboard in real time, and every transaction generates an FTA-compliant VAT receipt automatically.

For fine dining cafes and restaurants already running Foodics or Syrve, Fortis Table Pay adds a QR-based pay-at-table layer, letting guests view the bill, split, tip, and pay from their phones, while staff manage the same flow from the card machine.

Conclusion

A POS payment is the moment your business gets paid. Getting that moment right, fast, compliant, and connected to the rest of your operations, determines how cleanly everything else runs.

For UAE SMEs in F&B, retail, and services, the practical goal is a setup where the payment terminal and POS software are not two separate systems creating two separate data streams. The closer those two functions are to being the same thing, the less admin you carry, and the more confident your VAT reporting becomes.

You can explore how unified POS solutions like Fortis SmartPOS work in practice through our SmartPOS product page.

Frequently Asked Questions

- What is the difference between a POS payment and a card payment?

A card payment is one type of POS payment. POS payments cover any transaction completed at a physical point of sale, including card (chip & PIN or contactless), digital wallets, cash, and QR-based payments. Card payment refers specifically to the method; POS payment refers to the broader transaction type.

- Is POS payment safe in the UAE?

Yes. POS payments in the UAE process through regulated acquirers and card networks. Contactless and digital wallet transactions use tokenisation, meaning your actual card number is never transmitted. The UAE Central Bank maintains strict standards for payment security across all licensed acquirers.

- Do I need a POS system to accept payments?

No. You can accept card payments with a bank-issued terminal alone. However, a POS system helps you record sales, issue VAT-compliant invoices, track inventory, and reduce manual reporting errors. For VAT-registered UAE businesses, compliant tax invoices are mandatory, but the POS system itself is not legally required.

- Can POS payments handle VAT automatically?

They can, if your POS system is configured for UAE VAT compliance. A good system applies 5% VAT to every sale, itemises it on the receipt, and gives you export-ready data for quarterly FTA filing. If your terminal is bank-issued with no POS software layer, VAT handling is manual, which creates compliance risk.

- What happens if a POS payment is declined?

A declined transaction means the customer's issuing bank rejected the authorisation request. Common reasons include insufficient funds, a flagged transaction, or an expired card. The terminal displays "Declined" and no funds are transferred. The customer should try a different card or payment method. No charge is applied to their account for a declined transaction.